2011 FLORIDA LEGISLATURE

2011 FLORIDA LEGISLATURE

In 2011 a new insurance bill passed in the Florida Legislature that redefines sinkhole insurance coverage. Due to the high number of fraudulent cases of sinkhole activity and the difficulties of verifying sinkhole related damage the legislation was rewritten in 2011.

The new legislation has made sinkhole insurance for homeowners optional or a separate rider on their home insurance policy. On the other side of the fence, the insurance companies are not required provide coverage as they are allowed to opt out entirely. Now each policyholder needs to determine if sink hole coverage is worth the risk since the new requirements of what constitutes a sinkhole are much more strict.

Please see below for more detail regarding the 2011 Legislature:

According to Chapter 627.706

(1)(a) Every insurer authorized to transact property insurance in this state must provide coverage for a catastrophic ground cover collapse.

(a) “Catastrophic ground cover collapse” means geological activity that results in all the following:

1. The abrupt collapse of the ground cover;

2. A depression in the ground cover clearly visible to the naked eye;

3. Structural damage to the covered building, including the foundation; and

4. The insured structure being condemned and ordered to be vacated by the governmental agency authorized by law to issue such an order for that structure.

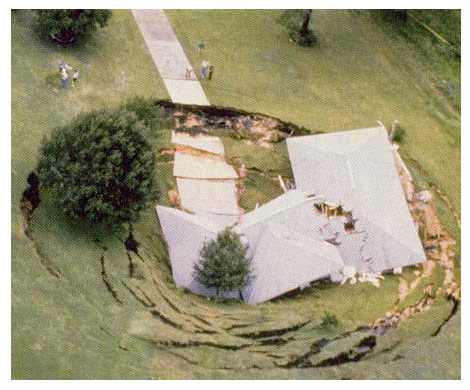

(h) “Sinkhole” means a landform created by subsidence of soil, sediment, or rock as underlying strata are dissolved by groundwater. A sinkhole forms by collapse into subterranean voids created by dissolution of limestone or dolostone or by subsidence as these strata are dissolved.

(i) “Sinkhole activity” means settlement or systematic weakening of the earth supporting the covered building only if the settlement or systematic weakening results from contemporaneous movement or raveling of soils, sediments, or rock materials into subterranean voids created by the effect of water on a limestone or similar rock formation.

(j) “Sinkhole loss” means structural damage to the covered building, including the foundation, caused by sinkhole activity. Contents coverage and additional living expenses apply only if there is structural damage to the covered building caused by sinkhole activity.

(k) “Structural damage” means a covered building, regardless of the date of its construction, has experienced the following:

1-Interior floor displacement or deflection in excess of acceptable variances as defined in ACI 117-90 or the Florida Building Code, which results in settlement-related damage to the interior such that the interior building structure or members become unfit for service or represents a safety hazard as defined within the Florida Building Code;

2-Foundation displacement or deflection in excess of acceptable variances as defined in ACI 318-95 or the Florida Building Code, which results in settlement-related damage to the primary structural members or primary structural systems that prevents those members or systems from supporting the loads and forces they were designed to support to the extent that stresses in those primary structural members or primary structural systems exceeds one and one-third the nominal strength allowed under the Florida Building Code for new buildings of similar structure, purpose, or location;

3-Damage that results in listing, leaning, or buckling of the exterior load-bearing walls or other vertical primary structural members to such an extent that a plumb line passing through the center of gravity does not fall inside the middle one-third of the base as defined within the Florida Building Code;

4-Damage that results in the building, or any portion of the building containing primary structural members or primary structural systems, being significantly likely to imminently collapse because of the movement or instability of the ground within the influence zone of the supporting ground within the sheer plane necessary for the purpose of supporting such building as defined within the Florida Building Code; or

5-Damage occurring on or after October 15, 2005, that qualifies as “substantial structural damage” as defined in the Florida Building Code.